Financial decisions at the highest levels of wealth are rarely just about numbers. They often reflect deeper psychological patterns, risk perceptions, and behavioral habits that shape how billionaires respond to challenges.

The idea that Jeff Bezos may choose to absorb fines rather than adjust a financial “hedge” strategy raises an interesting question: why would someone with access to vast resources make that choice?

While the specifics of any individual case can vary, behavioral economics and decision-making psychology offer several explanations for why this kind of approach can occur among ultra-wealthy individuals.

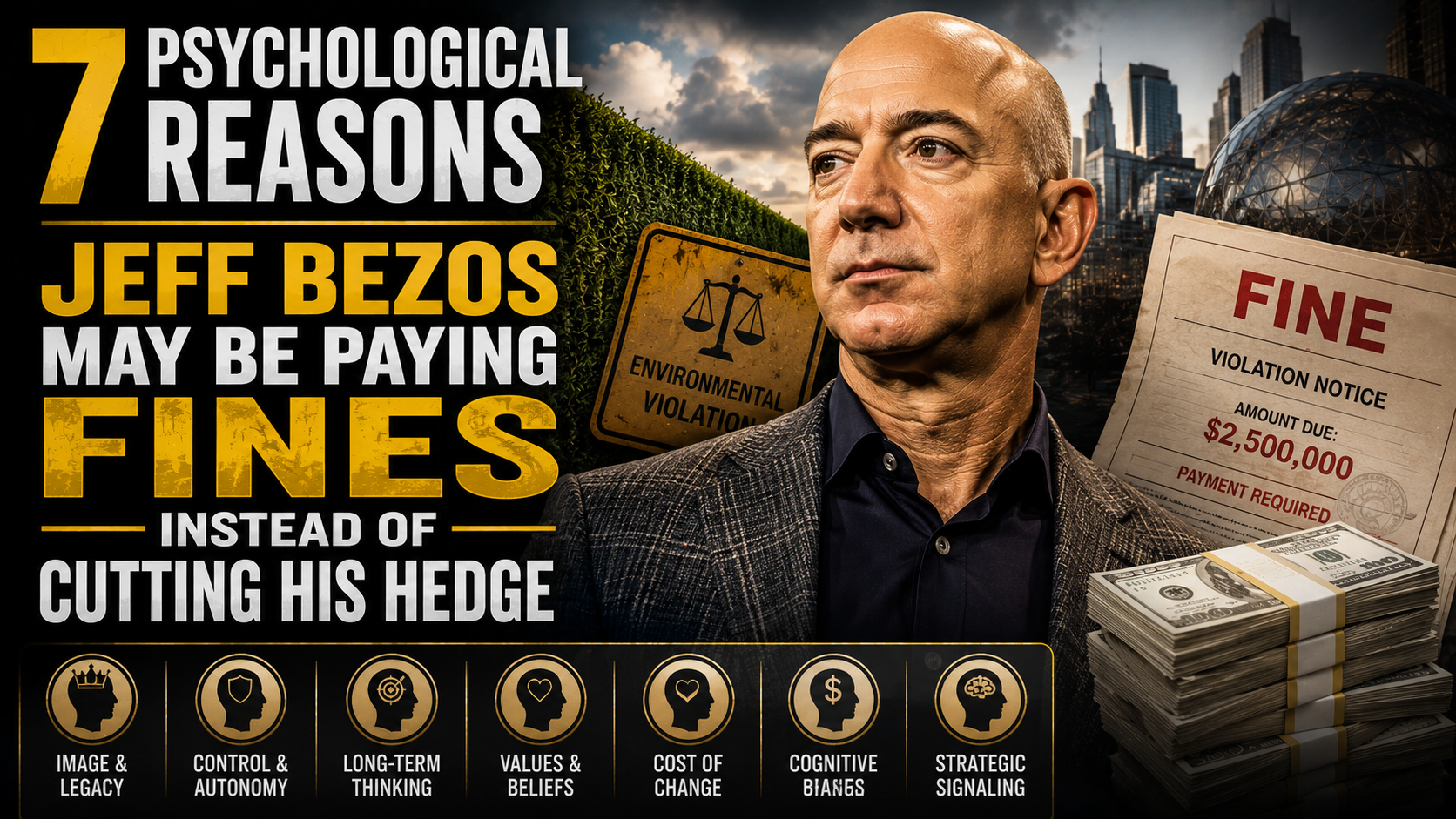

Here are seven psychological reasons that may help explain this type of financial behavior.

1. Loss Aversion and Perceived Trade-Offs

One of the strongest concepts in behavioral psychology is loss aversion—the idea that people feel losses more intensely than equivalent gains.

In high-level financial decisions, paying a predictable fine may feel more acceptable than altering a complex strategy that could introduce uncertainty or greater perceived losses.

Even if the math suggests otherwise, perception often drives behavior.

2. Preference for Predictability Over Adjustment

Large-scale financial structures are often built for stability.

Making adjustments to a hedge or financial position can introduce unpredictability, regulatory implications, or unintended consequences.

For some decision-makers, paying a known cost can feel safer than changing a system that already functions smoothly.

3. Cognitive Simplification in Complex Systems

Ultra-wealthy individuals often manage extremely complex portfolios.

In such environments, simplification becomes a psychological coping strategy.

Instead of continuously optimizing every variable, choosing a fixed cost like a fine may reduce mental load and decision fatigue.

4. Time Value of Attention

For individuals managing multiple businesses and investments, attention becomes one of the most valuable resources.

Adjusting financial strategies may require time-consuming analysis, legal consultation, and coordination across teams.

From a psychological standpoint, paying a fine can sometimes be viewed as “buying time” or preserving focus for higher-priority decisions.

5. Risk Tolerance and Strategic Prioritization

High-net-worth individuals often operate with different thresholds for risk compared to the general population.

What may appear inefficient externally can be viewed internally as an acceptable trade-off within a broader portfolio strategy.

In some cases, maintaining exposure or structure may be prioritized over minimizing smaller financial penalties.

6. Behavioral Anchoring to Existing Systems

Once a financial strategy is established, individuals and organizations tend to anchor to it.

This psychological bias makes people more likely to maintain existing systems even when adjustments might be beneficial.

Changing course requires not only financial calculation but also a mental shift away from established patterns.

7. Institutional Decision-Making and Delegation

At the billionaire level, many financial decisions are not made by one person alone.

Teams of advisors, legal experts, and portfolio managers often shape outcomes.

In such systems, decisions like paying fines instead of restructuring strategies may reflect institutional inertia rather than a single individual’s preference.

Understanding the Bigger Picture

While it can be tempting to interpret such financial decisions as purely personal choices, they are often the result of layered systems involving psychology, strategy, and delegation.

At the highest levels of wealth, decision-making is rarely simple. It is influenced by competing priorities, long-term planning horizons, and the desire to minimize disruption in complex financial ecosystems.

What looks inefficient from the outside may be viewed internally as a rational trade-off within a much larger strategy.

The Role of Behavioral Economics in Wealth Management

Behavioral economics helps explain why individuals do not always act in strictly “optimal” financial ways.

Biases such as loss aversion, anchoring, and mental accounting influence decisions even among highly educated and experienced financial actors.

These psychological tendencies become even more pronounced when decisions involve large sums of money and high uncertainty.

Efficiency vs. Stability in Financial Strategy

At the core of this discussion is a tension between efficiency and stability.

Optimizing every financial variable might appear ideal in theory.

However, maintaining stable systems often takes priority in practice, especially when changes could introduce risk or complexity.

This balance is a defining feature of high-level wealth management.

Final Thoughts

The idea of paying fines instead of restructuring financial strategies highlights how psychology can shape even the most sophisticated financial decisions.

Factors such as loss aversion, time management, cognitive load, and institutional delegation all play a role in how choices are made at the highest levels of wealth.

Rather than viewing such decisions as simple miscalculations, they are better understood as outcomes of complex human and organizational behavior operating under unique pressures.

In the end, wealth does not remove psychology from decision-making—it often amplifies it.